The Broker Is the Obstacle

How the Real–RE/MAX Deal Reveals a New Map of Power in Real Estate

Bottom Line

The reported $880 million combination of The Real Brokerage and RE/MAX Holdings is more than a consolidation event. It represents the alignment of two operating models built around a single idea: shift economic and operational power away from the broker and toward the agent.

Independently, each company proved that the thesis could scale. Together, they operationalize it.

But something else just happened.

For the first time, The Real Brokerage agent-first platform model has acquired what it has always lacked: a global consumer brand architecture.

That changes the competitive balance across the entire industry.

This Is Not Just a Deal. It Is a Design Choice.

At first glance, the transaction reads like a familiar story. A fast-growing, tech-forward brokerage pairs with a legacy global brand. Scale meets innovation. Balance sheet meets narrative.

That framing misses the point.

RE/MAX: The Original Assault on Broker Economics

Dave Liniger founded RE/MAX in 1973 on a single audacious premise: the high-producing agent was being systematically undercompensated by the traditional brokerage split model. His solution was the 100% commission concept. For a desk fee, agents kept everything they earned. The message was explicit and it was directed squarely at the producing agent. Your broker is keeping money that belongs to you.

That premise built an empire. RE/MAX grew into one of the most recognized real estate brands on the planet, with nearly 8,500 franchisees and global reach across 120 countries. But the growth was never built around the broker. It was built around the agent’s desire to escape broker economics.

The franchisee broker in the RE/MAX system was always a diminished figure. The brand, the training, the referral network, the tools all flowed top-down from corporate. The franchisee became an administrator. The franchise operator is the compliance officer. A flag-carrier. The RE/MAX system was engineered to minimize the broker’s value-add, because maximum broker value-add threatened the core business model.

What matters is not financial engineering. It is the operating philosophy both companies share. Each was built to solve what they viewed as the same structural flaw in real estate: the broker captures too much value relative to the services delivered.

Everything else follows from that premise.

- Compensation models were redesigned

- Technology became the delivery mechanism

- Brand shifted from brokerage identity to agent identity

- The broker’s role narrowed to compliance and supervision

The Real Brokerage Missing Piece: Consumer Brand Architecture

For decades, agent-centric models like The Real Brokerage and EXP have scaled by optimizing economics and systems. They are REMAX thinkers and operators without franchises, offices, consumer brands or leading consumer website portals. They have struggled against consumer brands.

Owning the consumer entry point.

- eXp Realty scaled globally without a dominant consumer destination

- The Real Brokerage built a modern technology platform but lacked brand gravity

That limitation forced dependence on agent-sourced business.

The addition of RE/MAX changes that equation.

- Global brand awareness

- A high-performing consumer destination in REMAX.com

- Decades of accumulated trust

- Motto Mortgage

This is not a marketing upgrade. It is a structural correction that gives agents new choices though The REAL Brokerage and REMAX offerings without looking away from their agent as the operator focus.

The Industry Is No Longer Organized by Brokerage Type

To understand the significance of this move, you need to zoom out.

The industry is reorganizing around four points of control.

- Who owns the agent

- Who owns the consumer

- Who owns the transaction

- Who owns the financing

Every major brokerage now sits somewhere along a spectrum defined by those control points.

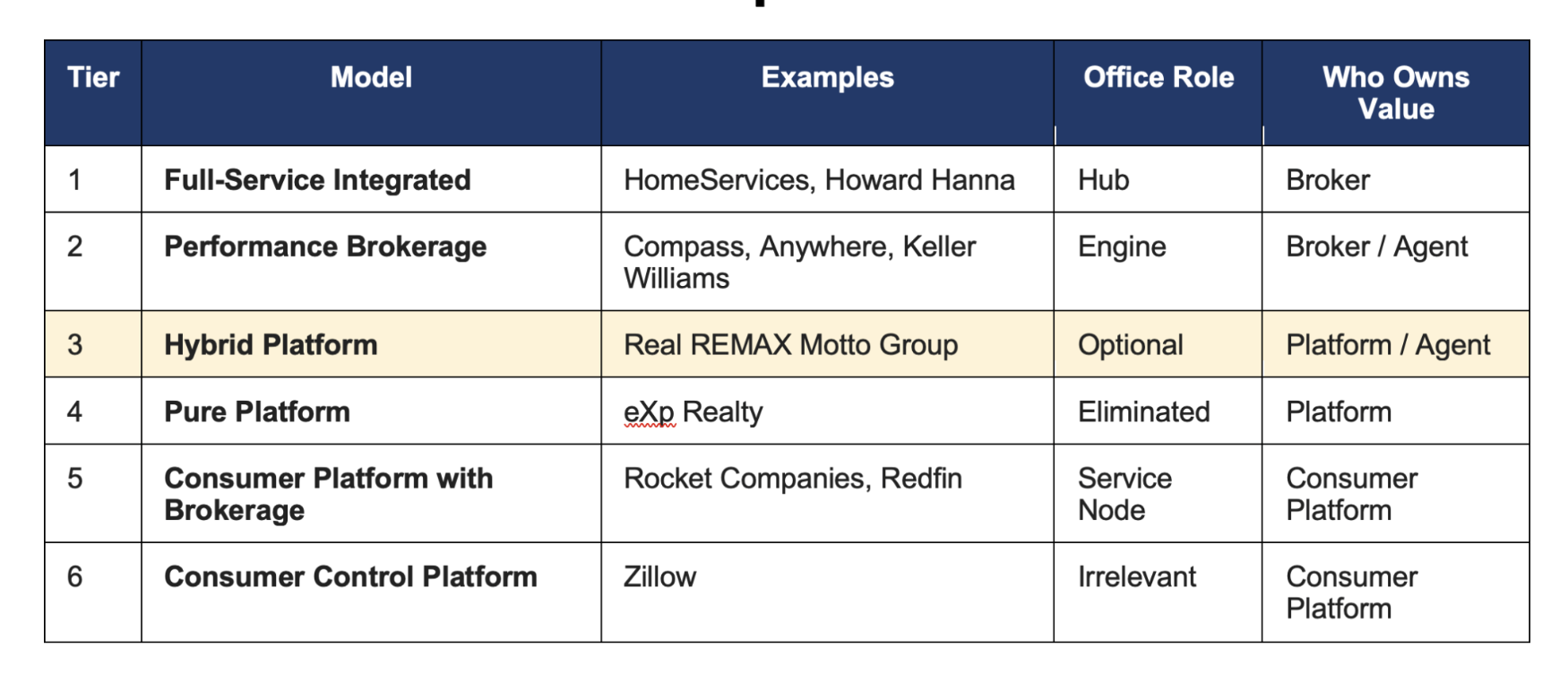

The Real Estate Control Spectrum

1. Full-Service Integrated Brokerage

Broker Owns the Transaction

- HomeServices of America

- Howard Hanna Real Estate Services

These firms anchor the traditional left side of full service companies. They integrate brokerage, mortgage, title, and insurance into a unified experience. Initiatives like OnePoint from BHHS reflect a deliberate strategy to own the entire consumer journey. Howard Hanna runs a similar playbook with their customer data platform that is unmatched.

Office Role: The office is the hub. It houses services, agents, and client interaction.

Strength: Maximum revenue per transaction and excellence of in person agent support and training.

Constraint: Harder to scale nationally because the culture is living in the offices.

2. Performance Brokerage

Broker Owns Agent Performance

- Compass

- Anywhere Real Estate

- Keller Williams

These firms invest in leadership, coaching, and culture.

Office Role: The office is the engine like traditional full service brokerages. It drives performance and accountability.

Strength: Builds high-performing agents.

Constraint: Weak penetration of mortgage, title, insurance offerings. The agent coordinates these services without a clear brokerage offering.

A notable shift is underway. Compass is increasingly borrowing consumer engagement through partnerships tied to Redfin and Rocket Companies. Even the strongest performance models now need external demand. KW partnered with Zillow, which burdens the transaction with the Zillow referral fee.

3. Hybrid Platform Brokerage

Platform Owns Operations, Brand Aggregates Consumers

- The Real Brokerage + RE/MAX + Motto Mortgage

This is the category being redefined by the deal.

Office Role: Optional. Symbolic. No longer central to productivity.

Strength: Combines platform scale with brand-driven demand.

Constraint: Execution. Brands must convert to engagement and REMAX agents will vote with their feet. If The Real Brokerage tech does not meet the agent standard, flight could occur. If REAL agents want offices, they can roll into a REMAX on Main St. across the world.

This is the first serious attempt to unify agent economics, platform infrastructure, and consumer brand at scale.

4. Pure Platform Brokerage

Platform Owns the Agent System

- eXp Realty

Office Role: Eliminated.

Strength: Scales faster than any other model.

Constraint: No centralized consumer entry point.

This model proved the broker could be minimized. It did not solve consumer aggregation. Agents partner with the portals they like and share commission with (I.e. Zillow, Homes.com, Realtor.com).

5. Consumer Platform with Brokerage

Platform Owns the Consumer, Monetizes Through Finance

- Rocket Companies/Redfin

These firms flipped the model.

They start with the consumer and monetize through mortgage and transaction flow.

Office Role: Service node. Supports fulfillment, not demand.

Strength: Controls demand and financing.

Constraint: Brokerage becomes margin-compressed.

6. Consumer Control Platform

Owns the First Click, Workflow, and Increasingly the Economics

- Zillow

Zillow sits at the far right.

It is a brokerage in license, but a platform in strategy.

- Leading consumer destination

- Showing infrastructure

- CRM layer

- Transaction visibility

- Mortgage through Zillow Home Loans

Office Role: Irrelevant.

Strength: Owns the first click and increasingly the financing moment.

Constraint: Must balance industry relationships and regulatory scrutiny.

The Two Moments That Matter

Across this spectrum, two control points define success.

The First Click

Who captures the consumer at the beginning of the journey? Is it the existing agent relationship or a website?

The Financing Moment

Who monetizes the transaction through mortgage.

- Integrated brokerages

- Zillow, Rocket, REAL

- Most others capture neither consistently

What the Real–RE/MAX Deal Changes

This transaction is about closing a gap.

Historically:

- Platform brokerages owned the agent

- Ecosystem brokerages owned the transaction

- Platforms like Zillow owned the consumer

Real is now attempting to bridge agent and consumer.

By acquiring RE/MAX, it gains:

- Immediate brand scale

- A global consumer entry point

- Credibility with buyers and sellers

- Motto Mortgage

If successful, it becomes the first platform brokerage that can compete meaningfully on both sides of the equation.

The Redefinition of the Broker

This is where the story comes full circle.

The broker is no longer the default center of the transaction.

The broker is now defined by the model they choose.

- Infrastructure broker: minimized

- Performance broker: amplified

- Ecosystem broker: expanded

- Platform broker: optional

- Consumer platform: bypassed

There is no single definition anymore.

Only positioning.

The Real Brokerage Story

Real REMAX Group will enter the market as the largest agent-direct platform ever assembled. More than 180,000 agents. 8,500 franchise offices. AI-powered transaction infrastructure. Global brand recognition. A combined revenue base of $2.3 billion.

Tamir Poleg will serve as Chairman and CEO of the combined entity, with three RE/MAX board members joining a ten-person board.

The deal is financed through a $550 million commitment from Morgan Stanley and Apollo Global to refinance RE/MAX’s existing debt and fund cash consideration. RE/MAX shareholders can elect $13.80 in cash per share or 5.152 shares of the combined company. Real shareholders will own approximately 59% of the new entity.

On the control spectrum, this places Real REMAX Group at Tier 3 with significant leverage to migrate further down the spectrum over time. The franchise offices will be rationalized. The 8,500 RE/MAX physical locations represent the single largest category of cost synergy available to the combined company. Expect a steady, multi-year reduction in the office footprint as Real’s platform-first operating model is imposed on the franchise network. The office is going from optional to symbolic to selectively eliminated.

The market’s initial reaction was instructive. RE/MAX shareholders celebrated. The stock jumped over 17% on the announcement. Real shareholders were less enthusiastic, with REMAX declining nearly 9%. RE/MAX investors believe they were rescued. Real investors are asking whether Poleg overpaid to acquire a declining franchise network.

Both reactions miss the strategic point. This is not a transaction about current value. It is a transaction about future recruitment capacity. Real acquired 50 years of brand equity, the thing it never had, and RE/MAX acquired the AI platform and growth narrative it was having a hard time communicating. The combination creates a recruitment machine unlike anything the industry has seen.

The Threat to Tier 1 and Tier 2 Brokerages

WAV Group has spent two decades documenting the evolution of the broker-agent relationship. The evidence is unambiguous. The traditional brokerage value proposition has eroded steadily as technology platforms have absorbed functions that brokers once owned. Training, marketing, transaction management, lead generation, and market intelligence have all migrated upstream toward the platform layer.

Real REMAX Group will combine the two most effective agent-recruitment narratives in the industry into a single pitch: the financial freedom of RE/MAX economics, the equity upside of Real’s ownership model, and the productivity power of AI-driven transaction tools. The agents most vulnerable to this pitch are not average producers. They are in your top 20%. The agents who already question what their brokerage does for them beyond a brand and a split.

These are agents who produce disproportionate transaction volume, who have the financial stability to make a move, and who have been asking the question that Real and RE/MAX have always answered first. What is my broker actually worth to me?

The defensible position is tier-specific. Tier 1 brokerages defend through service integration and the office as ecosystem hub. Tier 2 brokerages defend through coaching density, leadership presence, and the office as performance engine. The brokerages most at risk are those that occupy Tier 2 in name but operate as diminished Tier 3 platforms in practice. Brokerages that have hollowed out their broker function while still charging a Tier 2 split. Real REMAX Group will recruit your agents away one producer at a time, and the pitch will be devastatingly simple. We have the brand, the platform, the equity, and we cost less.

The real estate industry is moving from place-based value, to system-based value, to consumer-controlled value. Each model along the control spectrum makes a deliberate choice about the role of the office, and that choice reveals exactly where each company believes value lives. The broker is the obstacle only in the models that have already decided value lives somewhere else.

Dave Liniger built RE/MAX by telling agents that their broker was taking too much. Tamir Poleg built Real by telling agents the same thing with better technology and an equity certificate. The merger of these two companies is the largest single validation of that thesis in the history of organized real estate, and it places Real REMAX Group in the most strategically dangerous position on the spectrum: a Hybrid Platform Brokerage with global brand, AI infrastructure, and the recruitment capacity to migrate the industry’s best agents away from traditional brokerages one producer at a time.

The broker is not obsolete. Leadership, mentorship, local market authority, and genuine business partnership cannot be replicated by a platform, no matter how well-funded or AI-powered. But the broker who adds no measurable value to the agent’s professional life is about to find out, at scale and with urgency, exactly what the market thinks they are worth.

That reckoning is the real story of Real REMAX Group. The control spectrum is the map. The office is the signal. If REMAX agents don’t buy the technology story and The Real Brokerage does not operate remax.com effectively, this merger fails. And the agents are watching.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}