Every year, real estate sees the launch of beautiful products, offering awesome features, advantages, and benefits. Excellent marketing programs back them and the press creates a jubilee – Innovator of the Year!

Every year, real estate sees the launch of beautiful products, offering awesome features, advantages, and benefits. Excellent marketing programs back them and the press creates a jubilee – Innovator of the Year!

Then the product launches, and the industry shrugs its shoulder. It is the conundrum of new product development and innovation for real estate.

Most of these companies are doing everything right. They are doing research, spotting trends, holding focus groups, testing usability, and modeling lovely financials. If they can only get 1% adoption of this, or 3% of that, revenues will be awesome. There are 1 Million real estate agents; hundreds of thousands of brokers transacting trillions of dollars in transactions, buying $6 Billion dollars of technology in the United States alone! Wait until we go International! Canada is next!

For most innovators, this never happens. The drawing on the napkin was flawed.

What did they miss? Surely such a great product should have found success by accident. So, they go after it again. They get a few customers with a great social media-marketing program. Really connect with a group of excited agent and broker evangelists, hit a couple of more trade shows announcing how the early adopters are crushing it.

More shoulder shrugging.

Many outsiders look at the real estate industry and believe that it is ripe for disruption. It looks old. It looks slow. It looks easy. When you contrast the real estate industry with other industries, all of the foundational elements that trigger change and give birth to disruption are there.

The industry really has not changed, ever. Sure, there was that shift from MLS books to electronic MLS; from newspaper advertising to website advertising; from chasing keys to lockboxes; and from paper forms to electronic forms. That is really about all that has changed. Innovation has happened very slowly and only because……

Here is what industry veterans know. For a new product to be adopted in the real estate industry, the customer must be willing to take the risk to change. And yes, every change from an existing product or service to a new product has embedded risks. Change hurts.

There are three risks in particular that must be addressed when introducing a new product or service into the real estate marketplace. Clearly the product or service must offer equivalent benefits at a much lower price; or, offer new and improved capabilities at the same value proposition. Moreover, it must be backed by unbelievable customer support and training. If you’ve achieved these offerings then you have won a seat at the table. You must then overcome the risks that customers perceive in any new product or service:

- How do we get customers to use it?

- Will it be compatible with all of their existing workflows?

- Does it do everything the old solution did and more?

No matter how well the idea ranks in evaluation frameworks, the customer is seeking products and services to make their job faster, better, cheaper. If your idea achieves those goals, that’s table stakes. If your idea is difficult to adopt, requires significant change, forces the customer to acquire education or more knowledge in order to use the product effectively, then you’ve probably lost the game.

Inertia is probably one of the biggest barriers to new product or service adoption, and to overcome inertia the customer bases has to recognize that a new product or service offers very enhanced benefits, and doesn’t create a lot of work for a customer in order to switch and adopt. The more work the customer has to take on to adopt the new product or service, the better the benefits had better be. This is why even great new solutions often aren’t quickly adopted; the inertia level and adoption effort is simply too high, even for a product that offers compelling new benefits.

Here is a prime example. An MLS runs a new MLS system in parallel for 90 days so that agents can become familiar with the new system before the old system is turned off. 15% of agents actually try the new system before the cut over. 5% take the training course. The old MLS system is turned off. Everyone acts surprised and complains. The new system is better, faster, cheaper, has awesome support, training videos, it even washes your car every day and your dog comes home.

Most agents will like the old system better. The old system was not easier to use. They used it so it was easier to understand how to use. The new system is easier to use, but the agents just don’t know it yet.

Beyond forcing the customer to change in the adoption of a new product or service, there’s another significant question – does the product or service “work” with the existing infrastructure of operating systems, conventions, protocols and other expected and long held agreements? New MLS systems usually break every agent and broker website, in-house reporting system, data feeds, virtual tours, CMA software, Market Reporting tools, and more.

If a new product offers compelling functionality but does not work well within the rest of the customer’s solution set or needs, it sucks. Far too often, innovators dream of “disruption” but don’t understand the power of compatibility. RETS is a standard, right? If my product works in MLS A, it should work in every MLS. If my product gets approved in MLS A, it will be approved in every MLS. If this large broker loves it, all large brokers will love it. If this agent doubles their business in year, all agents will buy it. Right?

Every product or service is launched in a market where thousands of formal and informal agreements, standards, conventions and protocols exist. No matter how compelling your product or service is, it had better be compatible with the existing infrastructure or offer so much value that it can force the rebuild of the current infrastructure from the ground up.

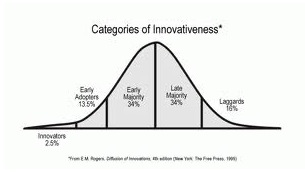

Technology innovators are often the “early adopters,” and as such we expect others to be early adopters as well. When Geoffrey Moore wrote about Crossing the Chasm, he wasn’t talking only to large corporate entities but also to every innovator. In the long run it does not matter how much the early adopters love your innovation, if the product or service can’t cross over to the early majority. And what the early majority wants is “completeness” or what Moore called the “Whole Product”. The difference between an early adopter and the early majority is that both are interested in new solutions, but early adopters are willing to try products that don’t quite have a support strategy, or perhaps don’t have all the documentation complete. Early majority, on the other hand, wants new technologies but wants the entire “augmented” product in place – support, communities, online and offline resources, channels, training, accessories and so forth. Without this “whole product” the early majority isn’t going to bite, no matter how compelling the new product or technology appears to be.

The core customer in real estate is 55-60 years old. Enough said.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

In the spirit of 60 Minutes – Point/Counter point and Saturday Night Live (for those old enough to remember Dan Aykroyd and Jane Curtin’s version) 🙂

Victor, I agree with your fundamental notions as to why change happens, and I often point out how pain causes change and that change is hard and that new product introductions have to solve a pain, be faster, cheaper etc. But, your blog got me thinking about how much really has changed in the real estate world. I think there has actually been huge change in our industry, that products are being adopted and innovation is taking place in a relatively short period of time. Maybe it’s from being in the business for over 25 years and being old enough to have watched the changes personally (and Aykroyd and Curtin on Saturday Night Live!) but I think you are mixing up “technology adoption” which does happen all the time, with the notion that innovation should change the underlying process. The title of the post, “Innovation Fails to Change Real Estate” implies that innovation “should” change the real estate process. That may make sense in some areas, for sure everything can be improved, but I think innovation can happen without a complete overhaul and that it has and is. I think innovation should make the real estate process more efficient for everyone from the broker to the consumer but having seen first hand how real estate is handled in many other countries I would also point out that it works fine here, in fact the best anywhere. I think innovation has taken place in many, many ways in our industry and in our technology but perhaps we need to stretch the review window just a bit wider in terms of time. Yes, our industry may be slower to make radical change in technology on a year to year basis but why should it? When MLSs install systems they hope that it is not for three years so they can change again. Why should they? That is not smart innovation, that is fixing something that isn’t broken! Does this mean they don’t embrace technology, no of course not. I also don’t think it’s just an age issue. The fact is, these systems work and you are right, nobody likes to change if they don’t have to or if, as you say the benefits are not really significant.

Take a look at what has really changed in our industry though over the last ten years and I think it is pretty apparent that our industry has in fact adopted multiple new technologies and that many technology innovators have made successful inroads. If you also look at consumer behavior in the real estate process you see that it too has changed incredibly. The dynamic between agent and consumer is totally different today than it was 10 years ago. That is huge innovation.

You are definitely right when you say the majority of new vendors don’t get significant market share out of the box but this is nothing new, adoption has always been like this in every industry. But if you look at 3rd party websites, data syndicators, MLS companies that started with an Internet version, IDX providers, Lead Generation companies, CRM products, new Transaction/collaboration models, Broker Enterprise software vendors you will see numerous companies that rode innovation and technology shifts to notable market share in the real estate industry in the last 10 years. If you look at changes in the real estate process in general, things like auto search and consumer portals on every MLS system, as well as just the availability of data, it points to huge innovation in our industry. To your comment on what the “early majority” want in terms of the full process, I think the mentioned technologies are pretty good examples where these keys are in place. They have support, communities, online and offline resources, channels, training, accessories and so forth. I think sometimes we miss how quickly these have all come together to form “full solutions” and gain real market share because we are looking at the new crop of new innovators that don’t have it yet and we have become an impatient world. We want change “now” and so we measure change and adoption in timeframes and snapshots that may not capture real movement and innovation adoption.

To me these technologies and “process changes” show real innovation that has been adopted by those involved in the real estate process. Has it changed the underlying process of how real estate is bought and sold at it’s core…no…but why should it….that works. It isn’t perfect, but it is better than anywhere else in the world.

So to conclude this rambling, I think innovation is taking place. I think key innovators are making significant progress. I think we see the agent/consumer dynamic has changed radically as has the broker/agent relationship and that technologies have been totally adopted that support these changes. I think innovation is being driven both within our industry from our older agent population and also from the real “core customers” in real estate, the buyers and sellers who are in the 35 – 45 age group that demand these changes. But, like everything in our world, we tend to look at everything in the timeframe of “soundbites” and “blogs’, and we tend to lose the forest from the trees. I think if we step back a few feet and expand our view a few years our industry has changed dramatically and the innovation is in full swing. Whether we like the ways it is changing, that is an entirely different question. Thanks for the great post Victor to get my mind running this morning!

Actually in recent surveys we have completed for MLSs, 40% or more are OVER 60, usually about 25% are over 70…..this is NOT the early adoptor audience….Technology companies have to be very cognizant of the reality of this target audience when they try to implement change…..a technology needs to be contemporary enough to make sense for the 20 and 30 somethings and yet be easy enough for the group that really runs the industry currently – those that think of technology as a necessary evil, not necessarily a tool for increased productivity and efficiency. Agents frame decisions in simple terms – will it help me sell more real estate? Then and only then will they consider it.

Technology has focused primarily on delivery of data, not on the basics of a real estate transaction which has not changed since the first cavemen exchanged caves. And no those cavemen are not on my board. 🙂

But the fundamentals of the real estate transaction boil down to the interaction between 2 parties – buyer/seller, agent/agent, broker/broker. Technology can assist with this, help speed some processes along, but at the end of the day it has nothing to do with technology, and everything to do with relationships.

As to market share of products i say if you can get 10-20% market share for your product you are doing great. In our market approximately 14% of the people do 90% of the business, with around 50% doing no business at all. Is that due to lack of technology or just too many people in the business?

You are 100% correct Russ. I would suggest that this is true in every market, in every MLS. As you know, there is little difference between Chicago and Los Angles – or the many other markets that you and your peers operate.

I am not sure that it is a problem either. The 50% of people that pay for services (and do not use them) support the productive agents by spreading out the costs of obtaining the technology that the MLS provides. Reduce the agent count by 50% and your costs will skyrocket. Perhaps this is a topic for another post about how the real estate industry needs to recruit more unproductive agents.

Here is a funny sidebar. I listen to the noise on Social Media websites when people are complaining about MLS services. The most vocal people on those websites are predominately people who are not productive agents. They play around on their computer all day talking to other (often unproductive) agents about best practices in real estate. Some are even social media experts and gurus. They have a real estate license and they pay dues, but are not bothering to do transactions. The issue is that they have nothing better to do than cause a big fuss around issues that do not impact them, and this causes real customer relations issues for the MLS leadership, staff, and board of directors. The noise can clog the productive workflow that you do. Not sure how to fix that yet, but I am thinking about it.

I completely agree Russ – given the complexity of the transaction and its impact on the quality of people’s lives (buyer/seller AND agent/agent), success has everything to do with (trust-based) relationships.

Therefore, the huge innovative changes we’ve seen in technology (and as Mike notes above, we have seen many) have impacted on the ease and efficiency of the process rather than fundamentally changed real estate.

Personally, I believe that many of the “innovator failures” (to deploy, to drive adoption, and to capture significant market share) are rooted in the fact that most of the innovators are rational technologists rather than trust-worthy relationship builders.

— Alon

If we were to double what we currently charge our customers would still only be paying around a dollar per day for the complete set of services provided, which is probably ranked lower than “other” on the list of expenses incurred by practitioners.

The other catch-22 we didn’t mention is that when products are rolled out MLS by MLS the vendor has the added cost of having to design for different MLS databases. This means costs are artificially higher and with only getting a 10% penetration in a market there is no hope of making money. Raise your price to cover your costs and the share goes down. This creates the famous product death spiral – remember the MLS book?

We need a standard database which theoretically could stimulate innovation and allow for nationwide sales rather than local.

You are right. Most vendors report that it costs about $1500 per market for integration with the MLS database. It is a one time fee, and a reasonable cost to “open a store.” On top of that, there is typically a data license fee which may range from $1,000 to $10,000 (our friend Greg Robertson loves this).

I do not think that start up fees for integration and data licensing are bad. I am sort of torn in my view. Clearly the MLS has a burden to service the vendor’s data needs on behalf of the participants and subscribers. The vendor is getting paid, but the MLS is not. Conversely, the argument is that any MLS fee to the vendor gets passed along to the participants and subscribers anyway. Regardless of your perspective, it costs money to assimilate and move data.

Sidebar: I like the RED Data Aggregation Model. They have aggregated data for their many IDX and VOW marketing across the nation. They are aggregating more as a result of their agreement with RPR. Homes.com, Wolfnet, iHomefinder, and others have done the same. Those companies normalize the data. In the case of RED, the normalized data may be provided as a service to other vendors with the proper contracts in place whereby the MLS approves. There is your standard database, and by the way – they are a RESO member.

Russ, I agree with the need for a standard database. Regardless of how they get the data, though, I would like to see the MLSs go to a straight profit share model (or at least a reasonable integration fee at start up) with the cost of integration built into the end cost. In this way the MLS decides on who gets to play in their sandbox and risk is shared but upside is also shared. Agents and brokers determine by use which products are chosen and this performance can be shared with other MLSs when making choices in their own market. Agents and brokers win hopefully by more product choice. I know many MLSs do have revenue share models today but it is all over the map. Start with a standard database though and it all gets much easier.

Interesting thought. I have always been a little concerned about this. In most MLS areas, if a broker selects a vendor for a product – the vendor gets a data feed. They sign a contract – they get a feed. The contract says what they can and cannot do with the data. How is that contract monitored and enforced beyond compliant display of data? What measures are in place that stop that vendor from selling the data out the back door, or preventing the data from being hacked and stolen? I have seen MLS data sitting on servers in a guy’s house.

Today, brokers are given a lot of latitude to select vendors without any qualifications. At least the vendor should provide proof of insurance and name the MLS as additional insured in case something happens. Alternatively, the MLS should do a little due diligence on these companies, or at least check their business license and credit. At a minimum, the master license agreement should be notarized.

Conceivably, someone could get on the phone and call a broker some-everywhere in America, provide fraudulent information about a new product that will make them millions; show them screenshots in a powerpoint; tell them they are a beta customer and that they will not be charged; email a few IDX agreements around for signatures; and get access to a data feed. Download all of the data and disappear. Right?